CONTACT US

PETITHAUSRC7155563

PetitHaus: Innovative housing solution that helps low/medium income earners access affordable, highly efficient qualitative living with convenience and unparalleled cost effectiveness.

Affordable Homeownership

SNEAK PEEK

This is a continuation of the previous post.

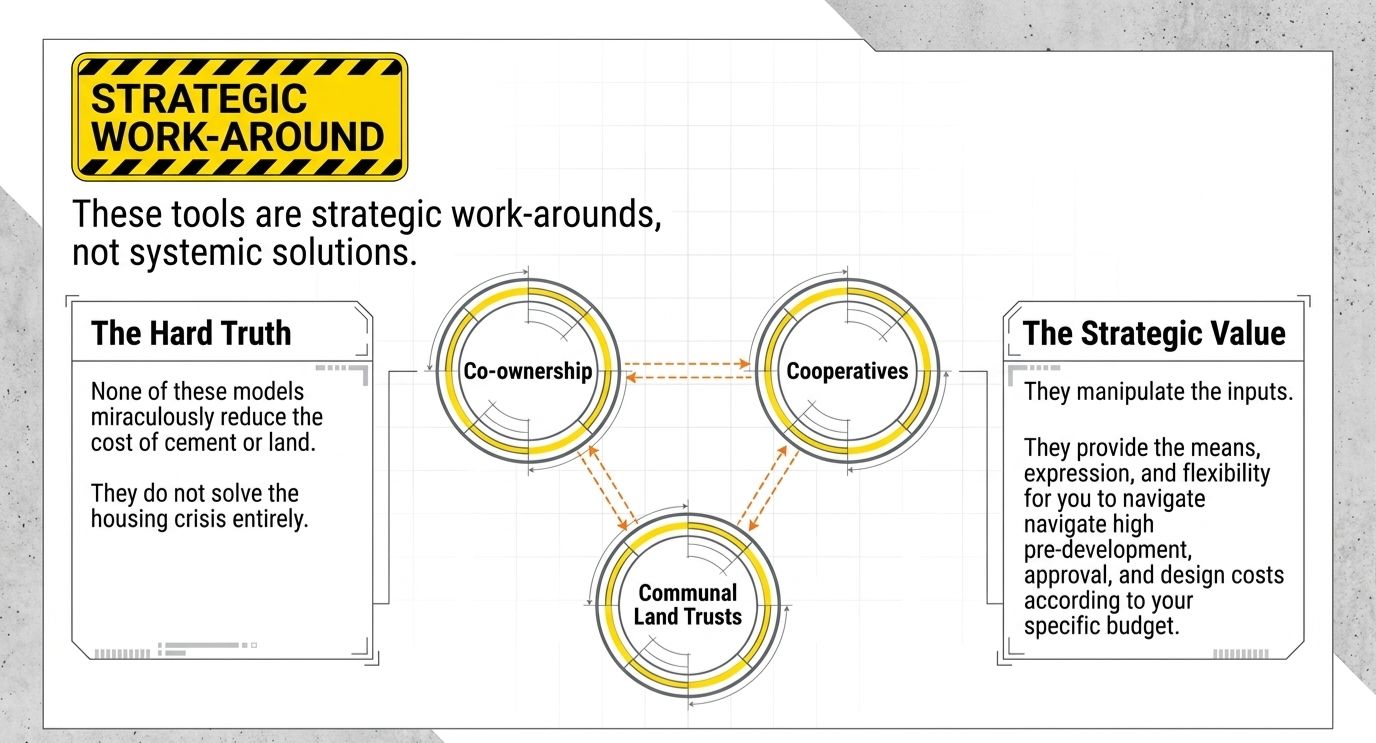

What we must admit about co-ownerships, cooperatives, communal living, and community land trusts is that they are still mere “work-around” tools.

And it's very necessary to say this because we must be very cautious about romanticising work-around solutions.

What these tools serve is to help people work around the rigidity of the housing market.

And maybe that distinction is all that makes building these tools worth it… Yet, all we can do is hope that they move the needle. Because none of these, by themselves, completely solve Nigeria’s housing crisis.

The reason is…

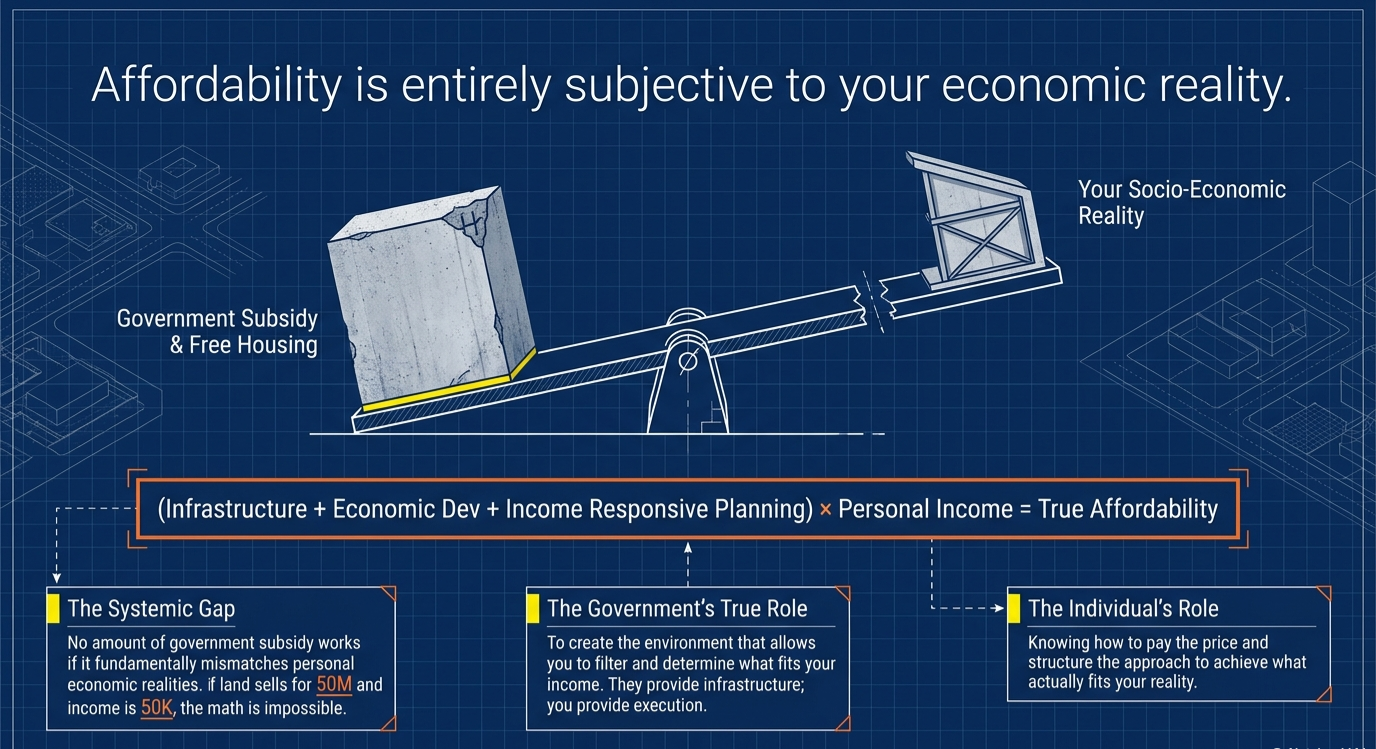

A ₦15 million “affordable housing unit” is still unaffordable to someone earning ₦120,000 monthly.

The only person that decides what’s “affordable“ is the person paying for it. Which means the government can not solve affordability by simply providing subsidies or building low-cost estates.

The real responsibility of the government is to create an environment where people can realistically decide what's affordable, and then meet it within their own economic realities.

That is, through…

Infrastructure | Economic empowerment | Income-responsive urban development.

… All 3 together. To structurally enable access to:

Now, here's a thing.

Having “dragged” the government for ages, without any meaningful outcomes, Nigerians have learnt to not wait until the government creates this “enabling environment". Most people seek workarounds to help them navigate ownership, albeit within the rigid market structure.

So let's zoom past “co-ownerships or cooperatives” for now and focus on...

Most would say: “To make housing cheaper.” But does it really?

This is perhaps the biggest misunderstanding about alternative housing solutions. People think “affordable” should mean that a 5-bedroom duplex is possible with ₦10 million.

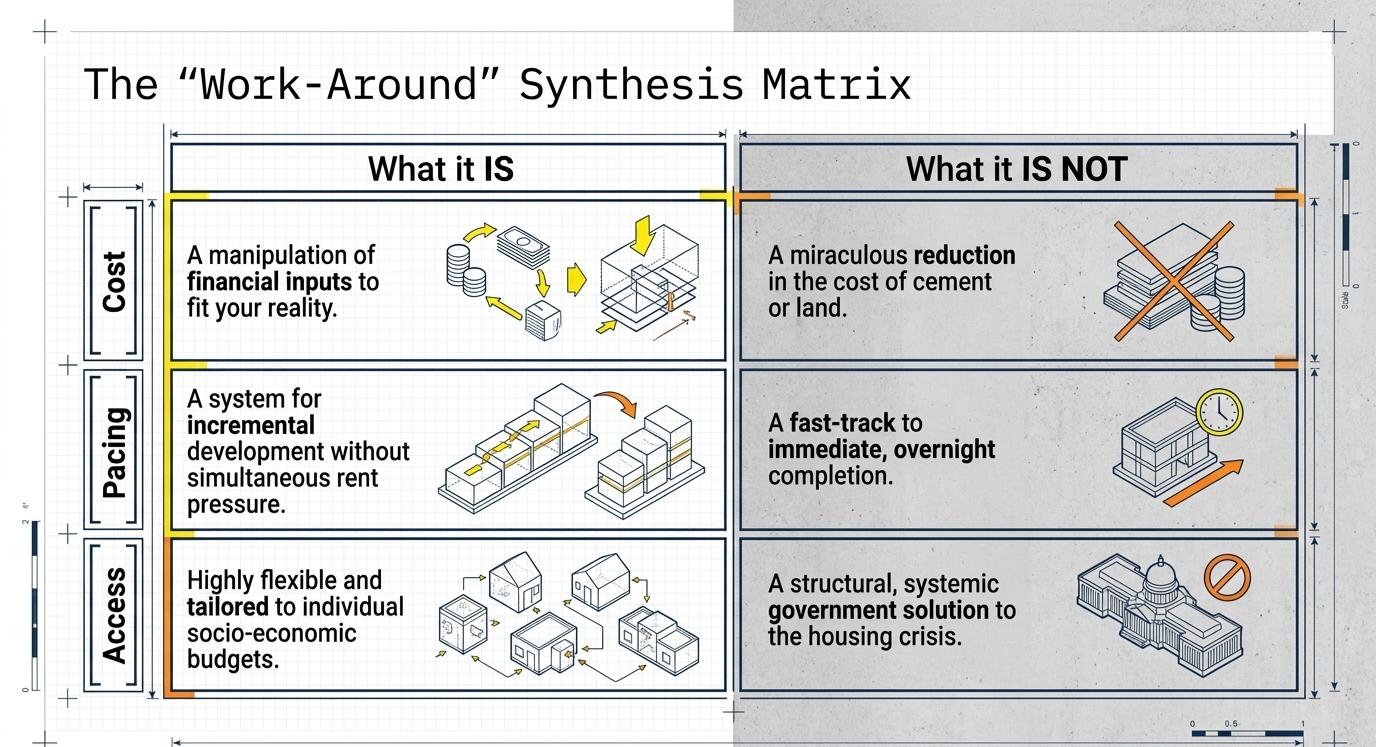

Yet, these solutions do not magically make cement cheaper. They do not suddenly reduce inflation. They do not crash land prices. They do not eliminate poverty.

What they really do is SIMPLY ease burdens… Create room to "breathe” inside a broken system. Help ordinary people navigate ownership, reduce entry barriers, spread costs, share risks, build incrementally… And adapt housing to their income realities. To reduce the financial pressure of trying to solve everything at once.

To allow people “plug themselves into” ownership at different levels. And create systems that allow ordinary people to participate in urban life without being financially crushed by it.

And that ‘easing the burden’ matters a lot more than we admit. Especially in an economy like ours, where…

But equally…

That has helped to power access to finance, which we can also leverage to create access to housing without high upfront commitments.

With these, helping people navigate housing will mean “rethinking housing efficiency". And affordable housing becomes more about “fluid neighbourhoods”...

A living ecosystem (built on social interaction) to leverage social capital as finance. A spatial community that balances privacy, affordability, and quality of life, for reclaiming urban equity.

One that facilitates housing at the cost-effectiveness of social housing while retaining personalisation... At scale, that is.

This brings me to 3 things that, no matter the tool or nomenclature… If we must redesign how we own, use, develop and transfer rights of property ownership affordably, remain non-negotiable.

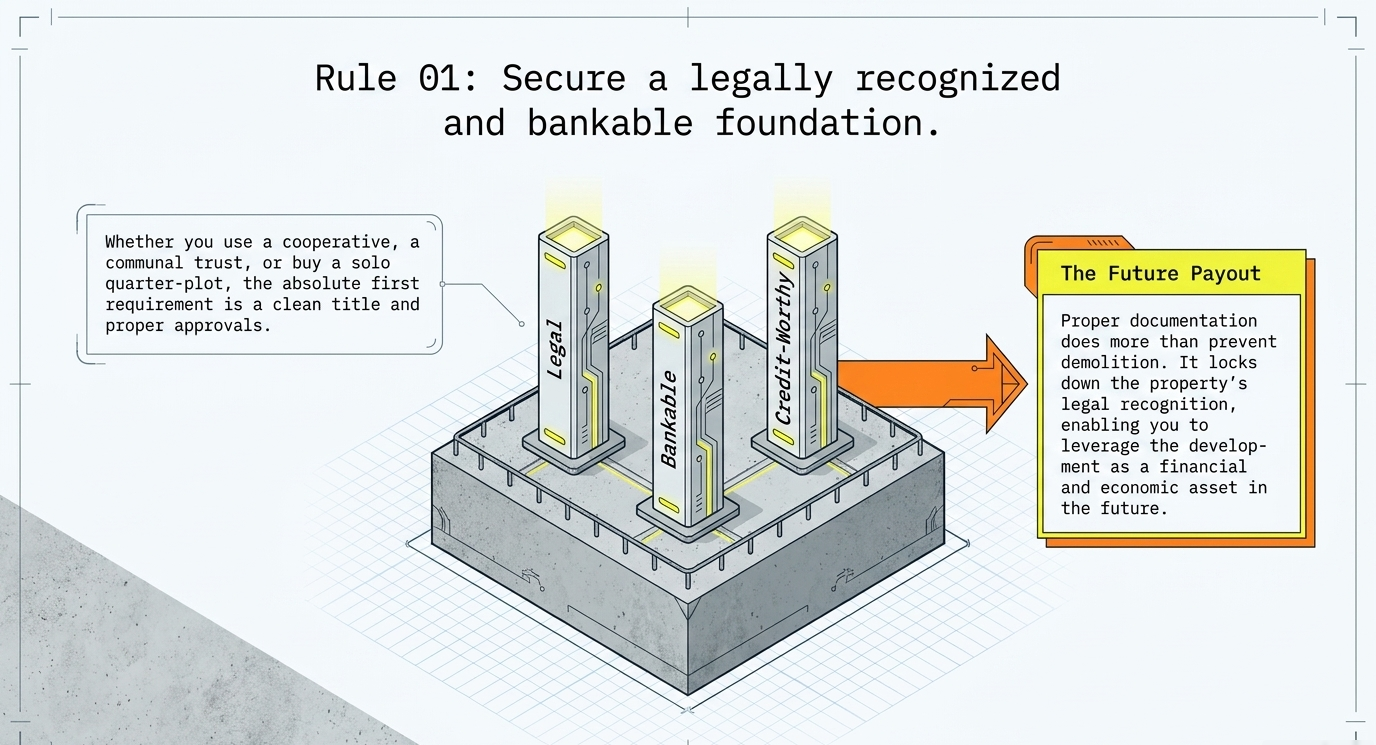

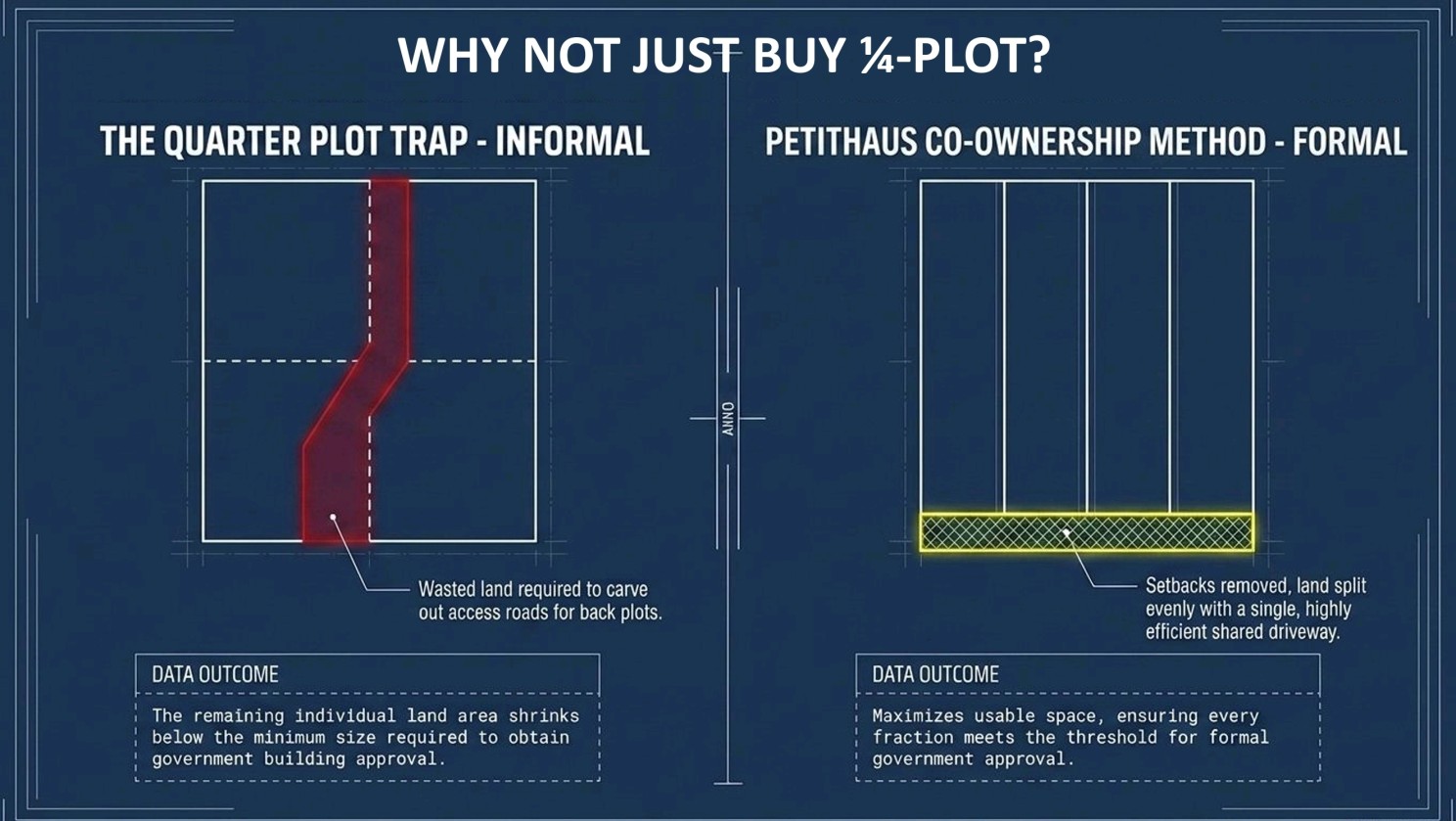

Whether you are buying through co-ownership, cooperatives, or even a quarter-plot arrangement… Make sure it is legally recognised.

Title. Documentation. Approval. Survey. Compliance.The true long-term power of property ownership for the underserved is not just ownership; it is also leverage. Therefore, a "legal, bankable & creditworthy" property becomes:

Without that legitimacy, any work-around further limits the future possibilities tied to the property.

This will offend many people. Yet...

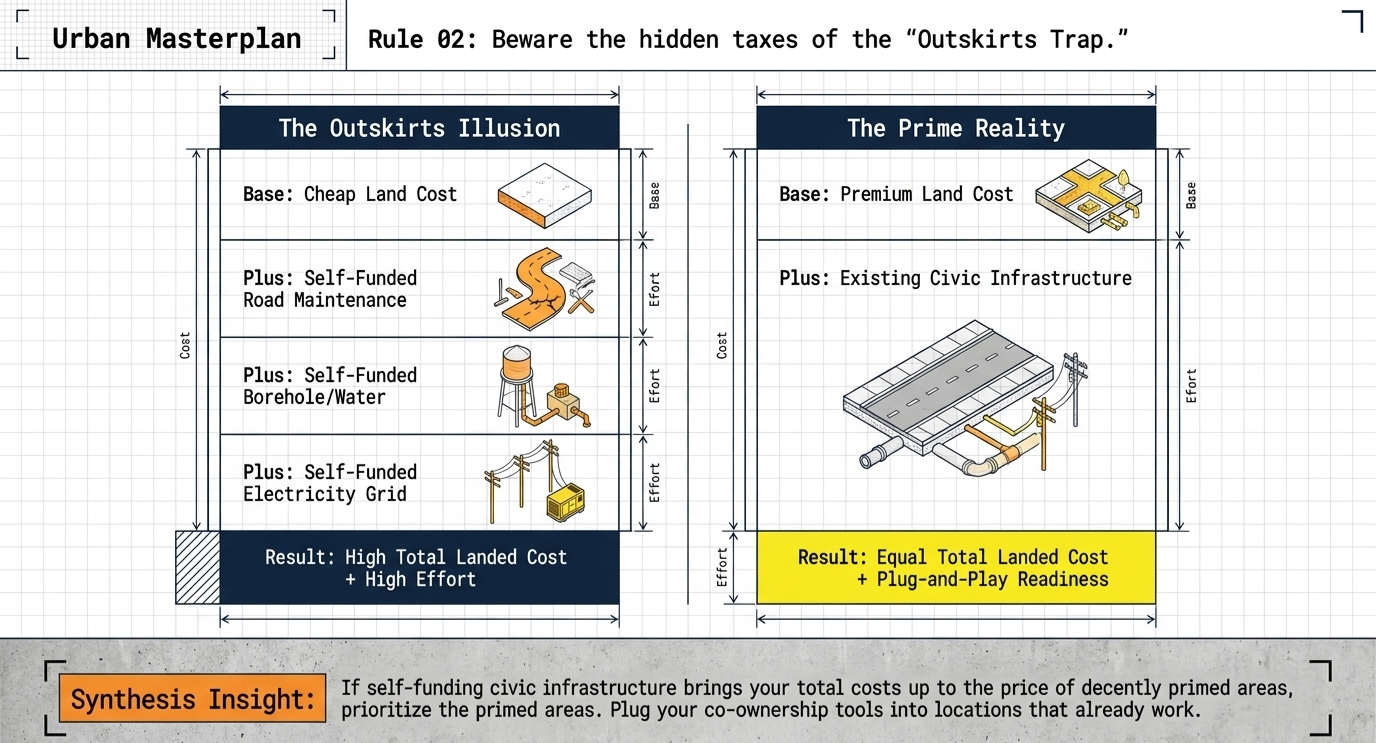

“Affordable” housing should not jeopardise your chance of unlocking and enjoying “location value”...

Yes, we understand the rationale, but many “cheap lands” are expensive traps. Acquisition may be cheaper, but after the extra “development levies” paid for infrastructure, housing costs almost as much as moderately prime areas.

Except now, you’ve also added long commutes, traffic stress, high transport expenses, isolation from opportunities, & loss of productive time.

So instead of chasing cheaper lands… Such work-arounds should figure out how to make existing urban areas accessible through smarter ownership models.

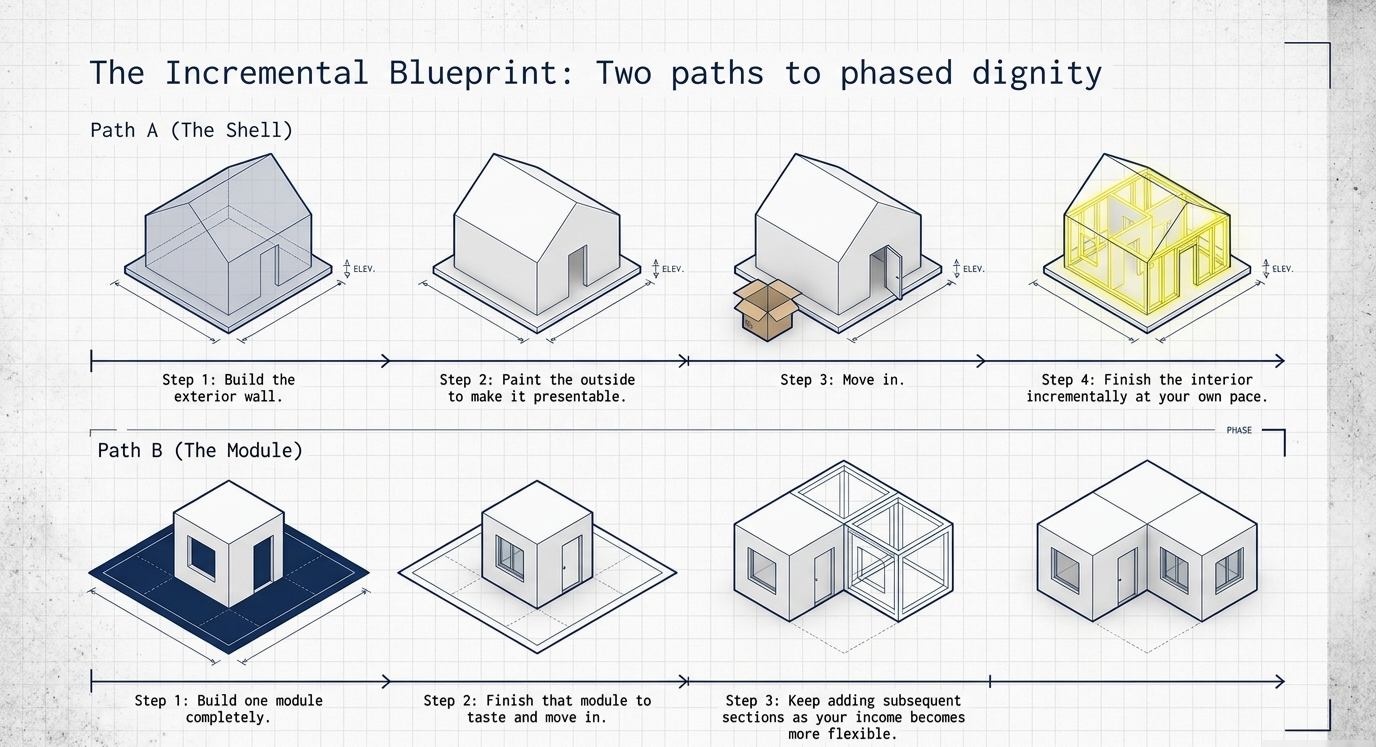

Housing does not always have to arrive fully complete in one expensive moment. Many Nigerians think living in an unfinished house is embarrassing. Meanwhile, globally, billions of people build incrementally.

Therefore, any workaround must incorporate flexibility for incrementality, adaptive construction, and organic development into ownership for you to truly adapt housing to your income realities.

With proper planning and technical guidance, incremental housing can still be dignified.

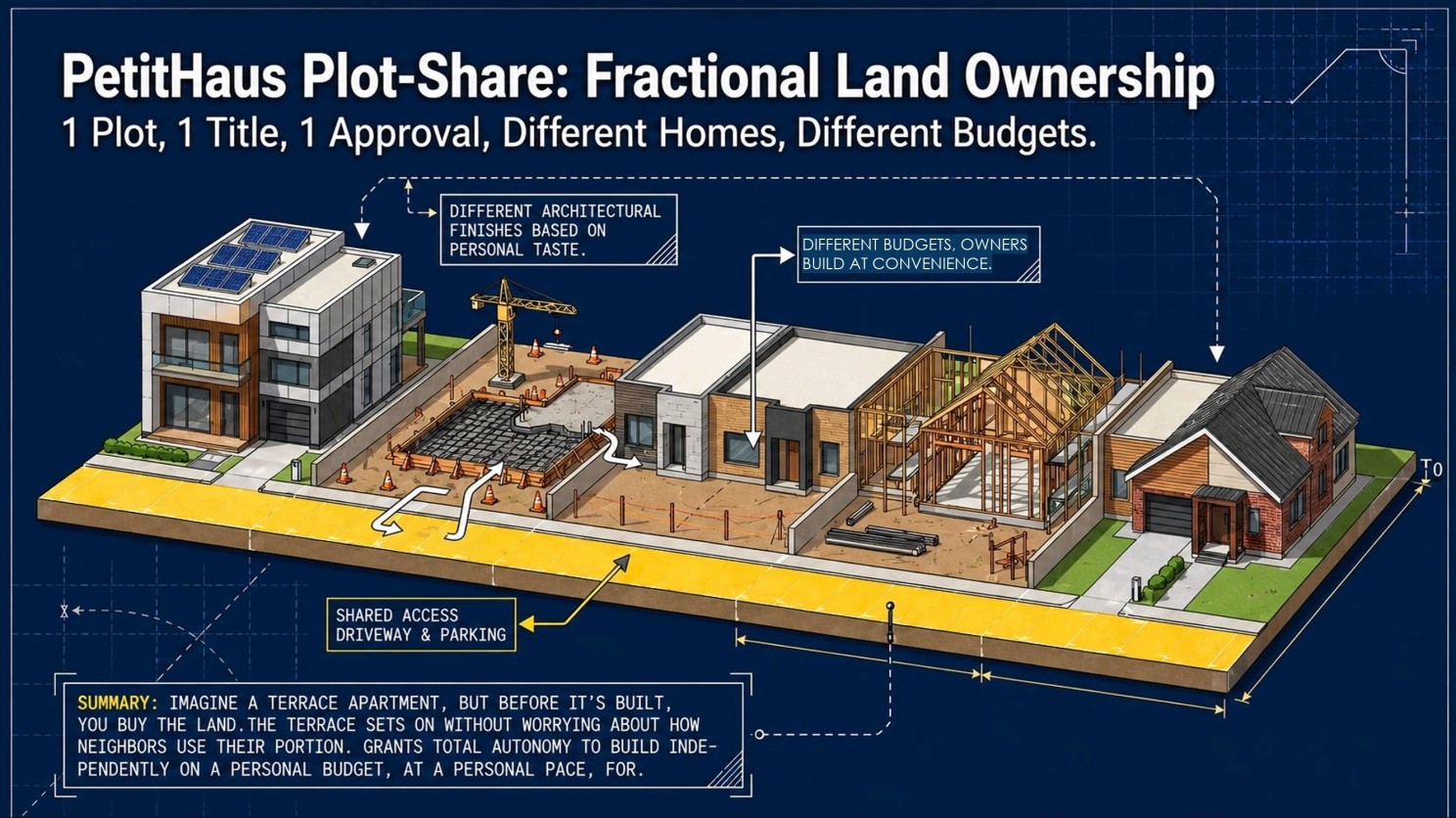

These are the biggest strengths of PetitHaus co-ownership structure. It allows people to build in phases without unbearable financial pressure.

This is where my strong belief in co-ownership as a more robust solution for the middle class to navigate the cost of home ownership as it fits their income comes in.

And it's the foundation on which we built PetitHaus Plot-Share, to help us intentionally enable urban access today and preserve urban equity for the coming generations.

Send a DM or reach out to explore this opportunity.

01.

02.

Category

Discover insights into creating affordable homeownership with PetitHaus.

.avif)