CONTACT US

PETITHAUSRC7155563

PetitHaus: Innovative housing solution that helps low/medium income earners access affordable, highly efficient qualitative living with convenience and unparalleled cost effectiveness.

Affordable Homeownership

SNEAK PEEK

Lagos is a city of living contrasts. Its advantage is equally a disadvantage.

It concentrates commerce, jobs, and upward mobility, but it also concentrates cost: expensive land, sky-high rents, and a city where proximity to opportunity can mean the difference between financial resilience and chronic debt.

Meanwhile, the traditional “build-and-sell” housing models and occasional government estates have not scaled to meet this reality. What happens is that most Lagosians are left to cobble together shelter through informal systems or accept long commutes to distant, low-amenity plots.

It’s time to rethink the supply side by starting with the one resource we already have in abundance: social capital.

The 'build-and-sell' is capital-intensive. Developers factor in land cost, financing, overhead, profit margins, and contingencies. End prices reflect market economics, not individual budgets.

Government programs often aim high but deliver low-reach outcomes because they’re one-size-fits-many, slow, and sometimes politically driven. Both pathways underserve the middle and informal sectors.

At its core, community-led housing means people who share a common interest use collective action to secure land, build homes, and manage assets on terms that reflect their incomes and priorities.

Community approaches allow buyers to choose entry points that match their cash flow and to build incrementally, avoiding the huge upfront costs that shut most people out. This isn’t a single model but a family of approaches allowing a blend of multiple informal solutions:

The defining features are pooled resources, local governance, phased building, and legal ownership for members.

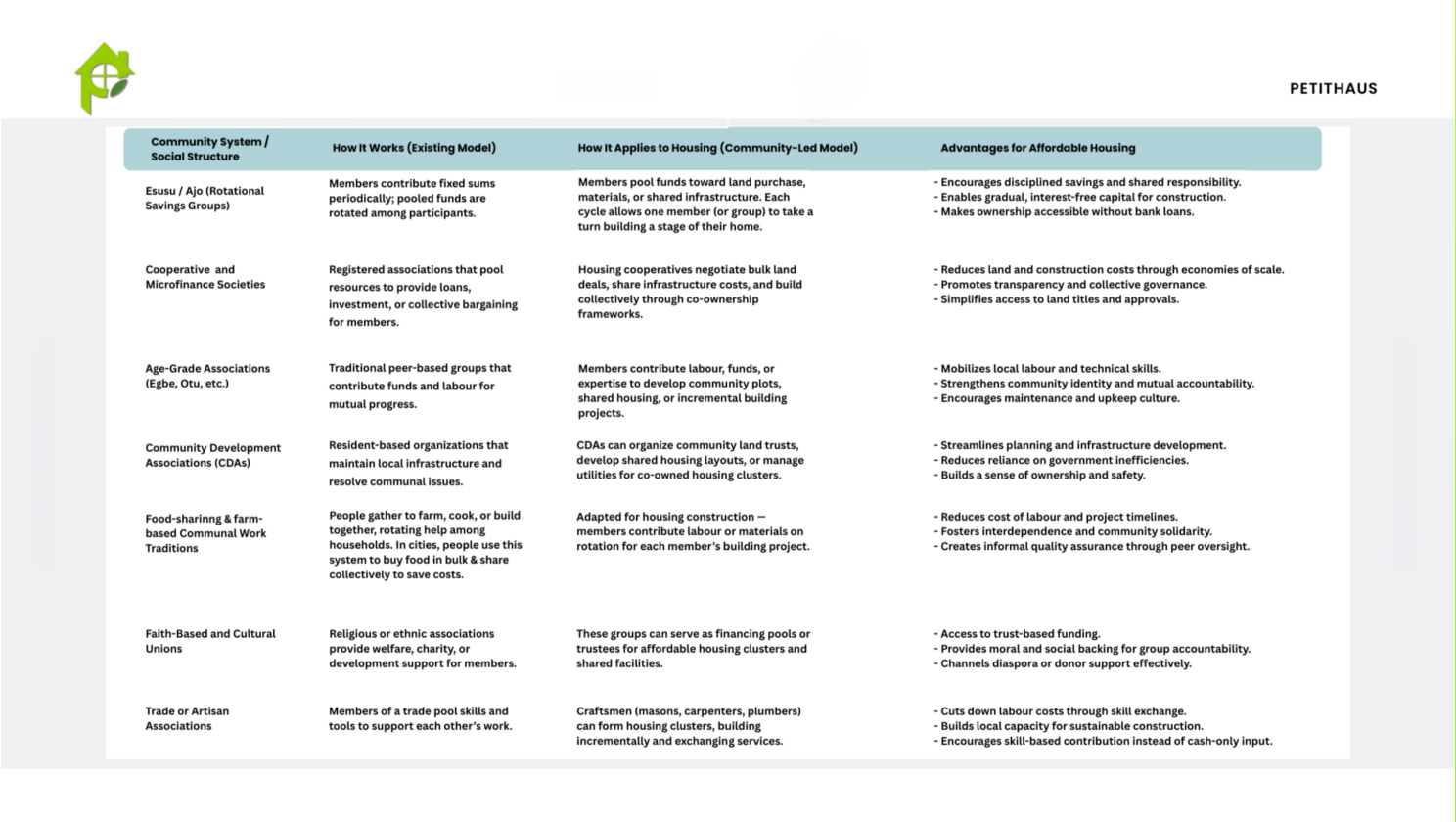

Across Lagos and Nigeria, informal savings groups, age grades, religious bodies, and cooperative societies already perform financial intermediation, solidarity lending, labour sharing, and collective risk management. These groups know how to:

Translating these strengths to housing simply means expanding the financial target from market trading and daily needs to land acquisition and construction. While adding legal scaffolding (titles, governance documents) so ownership is secure.

See the image below for more

Each model can be mixed. A cooperative might use esusu for deposits, then adopt a CLT framework to preserve affordability.

Community approaches reduce unit cost along three vectors:

The payoff isn’t instantaneous market parity; it’s a meaningful reduction in entry cost and greater predictability for families who can build gradually.

To scale safely, community projects must adopt transparent governance: member agreements, clear title plans, dispute resolution mechanisms, and professional oversight for technical and legal milestones.

Risk areas include land fraud, title disputes, and internal governance breakdowns. Access to basic legal services, affordable surveyors, and escrow arrangements mitigates these risks.

Want a practical example or step-by-step guide for a community group?

View and download this step-by-step template of the roadmap with a legal checklist of this community-led housing alternatives that is practical and easy to implement in Lagos

Community-led housing is simply a pragmatic adaptation. Using proven social systems but adding legal and technical scaffolding to create a path to scale affordability without depending solely on market or state largesse. For Lagos to unlock mass, livable, and proximate housing, policy must meet community energy halfway. Enabling title security, simplifying regulatory processes, and offering light finance.

If you’re already a member of a savings group, cooperative, or local association, the assets you need to own land may already be in your hands. Start the conversation. Organize. Build.

Want a ready checklist or a sample legal agreement for a 4- to 6-person structured fractional land co-ownership pool that saves you all the legwork?

We already built a platform to make that dream happen.

01.

02.

Category

Discover insights into creating affordable homeownership with PetitHaus.

.avif)